With an estimated 1 million people facing unemployment as a result of the current crisis it’s no wonder that the ability to service what is most household’s largest expense, mortgage repayments, will be placed under stress. If you’re in this precarious situation, or know someone else who might be, you may ask “what are the options and how does it work?”

Each lender has provided those in hardship with a six-month payment holiday. This article summarises the big four banks’ policy response but all lenders have implemented similar measures, with slight variations.

Commonwealth Bank

You will be able to defer home loan repayments for up to six months and, instead of making your repayments, interest will be capitalised, in other words, added to your loan balance. That balance will be recalculated at the end of the period and extended so repayments stay the same as they were before you started the deferral.

Westpac

You will be able to defer repayments for three months initially, with a possible extra three-month extension available after review. The deferred interest will be capitalised and when payments resume, they will increase slightly for the remainder of your loan term.

NAB

You will be able to defer your repayments for up to six month and there will be a three month ‘check in’ point with the bank. Like Westpac, the deferred interest will be capitalised and when they resume, payments will increase slightly for the remainder of your loan term. You will still be able to redraw during the repayment pause if you have made additional repayments to date.

ANZ

You may be able to put your repayments on hold for six months and interest will be capitalised. The bank will check in with you after three months and at the end of the period your minimum repayments will slightly increase to account for the increased loan balance.

What do I need to provide to have my payments suspended?

Again this will vary for each lender but in most cases you won’t have to provide any evidence that you’ve suffered substantial loss of income, or have contracted corona virus, but you may have to sign a declaration as such.

You should only defer mortgage payments if you really have to

It’s worth noting that there’s no advantage deferring the loan if in fact you can afford the repayments as capitalising the interest will mean that your repayments will increase over the life of the loan. For example, if you paused the interest repayments on a $300,000 loan with a current rate of 3%, after 6 months the balance of the loan will increase to $304,500. In most cases when you recommence your repayments, the minimum amount will be calculated based on this increased loan balance.

If you, or someone you know, unfortunately falls into this category you will need to contact your lender’s financial hardship team which can guide you through the application process. As always, please feel free to get in touch if we can assist in any way.

In the lead up to the last federal election the issue of first homeowner’s inability to enter the property market was poignant with voters and Scott Morrison released details of a new First Home Loan Deposit Scheme. From 1 January 2020, eligible Australian first home buyers with a 5% deposit can get home loans without lender’s mortgage insurance (LMI) through a government scheme.

Previously a borrower would need to save a 20% deposit in order to avoid paying LMI, which is an insurance, paid for by the borrower, to protect the lender against loss if the borrower defaults. If the lender is forced to sell the property and the full amount of the loan is not recovered, the insurance guarantees the difference. The additional expense of LMI has been a barrier to entering the property market in the past as, for example, the estimated LMI on a $400,000 property with a 5% deposit is around $12,700.

Whilst the first homeowner must still repay the full loan amount, the scheme allows them to enter the market earlier as they can spend less time saving for the deposit. This can be combined with other existing state-specific schemes such as the First Homeowners Grant (FHOG) and relevant stamp duty concessions.

The scheme is further restricted to:

Owner-occupied loans on a principal and interest repayment schedule

The applicant(s) cannot earn more than $125,000 a year as a single or $200,000 as a couple

Access to the scheme is limited to the first 10,000 applicants per year on a ‘first in first served’ basis.

The maximum value of the purchased home under the scheme varies by state to state and between city and regional areas.

Whether the scheme will in fact increase first homeowners’ access to the market is being widely debated. Arguments are focussed on whether those people who could benefit from access to this scheme may struggle to be able to gain approval for a loan of that size based on current banking regulations. The effectiveness of capping the scheme to 10,000 applicants has also been drawn into question as this only represents around 10 percent of all Australians who bought their first home last year. Banks have also indicated that they are considering charging higher interest rates for the applicable loans. Their justification is that a borrower who has only been able to save 5% is at greater risk of default than one who has displayed a better saving history and saved more. Only time will tell.

After nothing but negative headlines for months, since the re-election of the Liberal government there’s been a sharp about-face for the Australian property market. In quick succession the risk of doing away with negative gearing and halving the capital gains discount rate vanished, then the Reserve Bank governor flagged lower interest rates and then the banking regulator lowered the qualifying hurdle for borrowers.

So you’d think it should be happy days for potential property investors: saddle up and back to the races! Not so fast.

If you take the time to think things through, there are still plenty of warning signs, especially for those looking to buy a residential investment property in Melbourne or Sydney.

Speculating is not investing

CoreLogic reports the average gross rental yield for residential houses in Melbourne and Sydney is 3.6%. But to work out if that’s a good investment you have to deduct all your expenses to arrive at a net yield: that includes income tax, agent commission, land tax, body corporate fees, insurance, maintenance costs, and what have you. When we work out a client’s net yield it’s typically between zero and one percent.

By contrast, a six-month, government guaranteed term deposit currently pays you 2.5% gross. For someone on a 37% tax rate that’s 1.6% net, with no other costs to worry about.

When an asset is yielding less than what’s called the ‘risk free rate’ (and you don’t get much more risk-free than government guaranteed), the only way you can justify investing in it is making a capital gain, and, by definition, that makes it a speculative asset.

Compare assets

Commercial property on the east coast yields about 5.5% – that’s a 50% premium to the residential average. Don’t fall into the trap of saying, ‘but commercial property prices don’t go up as fast as residential’, remember we’re talking about investing here, not speculating.

The other classic growth asset is, of course, shares, and the most common valuation measure for shares is the price to earnings (PE) ratio, which is simply the price you pay divided by the net earnings you receive. At the moment the ASX200 is on a PE of 16.5, but for a rental property with a net yield of 1% that’s a PE of 100!

The only way you can explain that difference is debt, which always lies at the heart of every property boom, and that’s where the Australian residential property market looks really risky.

Too much debt

According to the Bank of International Settlements, at 120%, the ratio of Australia’s household debt to GDP is second only to Switzerland’s and compares to the average for developed economies of 72%. For context, to look at three other recent debt-driven housing booms, the same ratio for the US at the peak of its pre-GFC property boom was 99% (it’s now 76%), Ireland’s was 117% (now 44%), and Spain’s was 85% (now 60%).

The Reserve Bank reports Australian household debt to disposable income is now 190%, up from 160% in 2012 (and about 110% 20 years ago), yet only 37% of homes have a mortgage! Underlying that, in Sydney and Melbourne the loan to income multiple went from the old rule of thumb of three times, to now about six.

Again, for some perspective, Sydney’s house prices rose 80% between 2012 and the 2017 peak and Melbourne’s went up by 56%. By comparison, US house prices rose 78% over the five years to their peak in 2006, Ireland’s prices went up 100% in three years and Spain’s by 50% in four years. Now, about 18 months after they peaked, Sydney property prices are down 15% and Melbourne’s by 11%. From their peak to trough US prices fell 34%, Ireland’s 55% and Spain’s 35% and the average time from top to bottom was just short of six years.

Banks and incentives

To understand what’s going on in the housing market it helps to understand how we got here.

In 1988 the first Basel banking accord was released, which halved the capital banks had to keep on their balance sheet against residential mortgages. That meant the banks’ Return on Equity, or profitability, doubled overnight.

[Explainer: if a bank has to retain $20,000 of capital on its balance sheet against a $100,000 loan, on which it charges an interest rate of 5% per annum, its return on equity (ROE) is $5,000 (interest) on $20,000 (capital), so 25%. If the capital buffer is halved, it’s $5,000 on $10,000, so 50%. Bingo, the ROE doubles overnight.]

The Australian banks, coming off an existential crisis after over-lending to the ‘80s entrepreneurs like Bond and Skase, jumped on this newfound source of profitability so enthusiastically that our so-called ‘commercial banks’ have swung from housing being one-third of their loan books to now being two-thirds. That has required a 30 year, industrial scale campaign of shoving as much debt as they can into the sector, aided by tailwinds of declining interest rates, tweaking the tenure of loans from 20 years, to 25 and now 30, and the rocket fuel of interest only loans.

Why did they do that? Because it kept their profits high.

And the upshot? Over the last 10 years mortgage debt has grown at 7% per annum, while real wage growth has been 2.5%. In Melbourne, between 1960 to 1988 the multiple of average wages required to buy the median-priced home went from 2.8 to 3.9; but then between 1988 to 2018 it went from 3.9 to 10.3!

More debt in an over-indebted sector

The cheerleaders for the property market are back in force, but their assertion we’ve seen the bottom in house price declines is based entirely on more debt being taken on. That response is very much level one, or kneejerk, thinking: just because you’re able to buy a house doesn’t make it good value.

Clearly the Reserve Bank is worried about the effects of falling house prices on the broader economy: an Assistant Governor gave a speech chastising the banks for being ‘stingy’, they leaned on APRA to quietly reopen the interest only lending taps just before Christmas last year, they’re openly flagging lower interest rates and APRA’s eased up on the lending benchmarks the banks have to use. Every one of those actions is designed to throw more debt into an already over-indebted sector.

The cries of relief that negative gearing won’t be abolished also breaks another rule of sound investing: you never invest in an asset based on tax breaks. It should always stand on its own feet.

After 30 years of debt-fuelled rising property prices, the ‘anchoring bias’, where peoples’ expectations are shaped by past experience, will be hard to shake. But behavioural economics tells us as investors, our best decisions are made when you engage second-level thinking and look beyond your biases.

Some extra facts

* Debt-driven housing markets: have a good look at this chart and then ask yourself how it is Australian house prices could have gone up by so much more than per capita income. The answer is more and more debt.

*Dramatic fall in foreign buyers: Foreign Investment Review Board approvals of foreign residential real estate purchases for 2018 were one quarter of what they were in 2016.

*The crane index: Per Ashley Owen of Stanford Brown – In April 2019 there were 735 high rise cranes on the skylines of Australian cities, which was more than the whole of the USA. 72% of these cranes were for residential units, so the RBA’s long hoped for shift from residential to commercial and infrastructure had not happened. The last time one country dominated the world crane market was Dubai in 2010 and that ended in Dubai’s dramatic collapse and bailout. House prices in Dubai are still lower now than they were 10 years ago – and that’s before inflation.

*An increase in supply: in February, Core Logic reported there were more houses up for sale than at any time since 2012. With 115,000 houses listed across the country, it was 15% higher than the same time in 2018.

*Mortgage stress on the rise: in March 2019 S&P said the number of borrowers more than three months behind on their mortgage repayments doubled over the last decade, a sign of a “persistent rise” in the severity of home loan arrears. About 60 per cent of borrowers overdue in repayments are currently overdue by more than three months — this is up from 34 per cent a decade earlier.

*Australian banks are clamping down on how much they’ll lend…: in November 2017, the Commonwealth Bank’s “how much can I borrow” calculator estimated someone on the average annual salary at that time of $80,278 could have borrowed $463,000. By April 2019 that had dropped almost 25% to $351,100.

*…but it’s not a credit crunch, just sensible lending standards: the bank ‘lending crackdown’ is not a credit crunch, as some describe it, it’s actually a return to prudential lending standards that should never have changed in the first place. It was symptomatic of the banks’ enthusiasm to lend as much as possible for residential property, because of the high ROEs, that they were prepared to waive through loan applications that failed to properly assess a borrower’s spending.

Prior to that ‘crackdown’, instead of individually assessing a loan applicant’s spending, banks were frequently using the Household Expenditure Method (HEM), which presumes a certain level of spending based on postcode, the number of family members and salary. However, it was easy to fudge numbers and it could leave out critical amounts like school fees. At one point as many as 75% of loan applications relied on the HEM, which, if nothing else, is a reflection of how lazy the banks had become.

Indeed, at the height of the property boom in 2017, UBS did a survey of borrowers who’d taken out a mortgage in the previous 12 months, which found one-third of applications were not ‘factual and accurate’. Having done a similar survey in 2015 and 2016, which reached roughly similar conclusions, they estimated the banks had about $500 billion of factually inaccurate loans on their books, which became known as ‘Liar Loans’ in the US during the GFC.

Buying residential property in Melbourne has been a great way to make money, with an astonishing total return over the 31 years to 2016 of 11.2% per year. The problem is, the majority of that return was capital gain, and almost all of that gain was underwritten by buyers taking on more and more debt, to the point that Australian households are now the second most indebted in the world. At some point households simply won’t be able to take on more debt, and then what happens?

I know I’m venturing into an area where emotions can run high, partly because the average Australian has an awful lot at stake when it comes to property values. I’ll say up front I’m definitelynot advocating anybody rushes out and sells their property holdings, I’m simply offering some observations about residential property from an investment point of view. They may be right, or they might be way off the mark.

Property prices and debt

I don’t think it’s especially controversial to suggest there’s a logical relationship between the amount that people are prepared or able to borrow to buy property and how much they end up paying, but I reckon the two charts below kind of prove it.

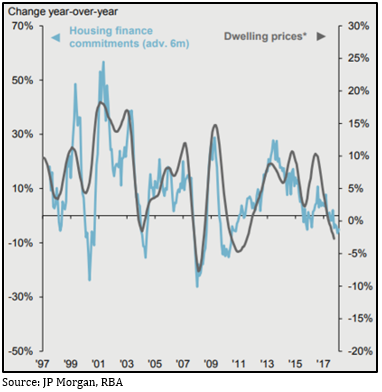

Chart 1: RBA data suggests house prices have risen in line with the amount of household debt

Chart 2: There’s also a close relationship between loan approvals and house price growth

Investing in property is, by definition, speculative

According to SQM the current ‘gross yield’, that’s the income you receive from rent before accounting for any taxes or costs, on Melbourne residential property is 2.9% per annum.

If you assume the property owner has a marginal tax rate of 37%, that brings it to an after-tax yield of 1.8%. Once you’ve accounted for all the other costs, such as management fees, body corporate fees, land tax, rates, insurances and what have you, you are very lucky to get a 1% ‘net yield’.

That same landlord could put their money in a term deposit paying 2.7% per annum; take out the 37% tax and the net yield is 1.7%, and there are no other costs to pay. Given that return is guaranteed by the government, we can call that the ‘risk-free rate of return’.

It’s a rock-solid law of investing that if the yield on an asset is less than the risk-free rate of return, then the investment is speculative, because the only way you can justify it is through capital gain. In other words, you’re banking on someone paying a higher price than you did.

Over the past 31 years, the capital gain on Melbourne housing has averaged 7.5% per year, so that speculative bet has been well rewarded, and it’s understandable for anybody to think that’s a well-established trend which is likely to keep going. The trouble is, it’s entirely reliant on people taking on more and more debt.

How expensive is residential property?

One way of working out the value of an investment is using what’s called a ‘price to earnings (PE) ratio’. That’s where you take the price of an asset and divide it by the earnings it generates per year; so if a $100 asset generates $10 of earnings per year, it’s $100 divided by $10, which gives you a PE ratio of 10 times.

The PE tells you how many years it would take for that investment to pay itself off and is effectively a measure of sentiment. If you’re pretty sceptical about an asset you’d want to get your money back sooner rather than later, so you might have a low PE of 4-5, but if you’re bullish on an asset you’ll be happier to have a higher PE.

You can use a PE ratio to measure the value of a share (it’s the share price divided by the earnings per share), or a property (the property value divided by the net yield). The current PE for the Australian share market is about 15 times. If we use the 1% net yield on property as above, that’s a PE of 100 (if you had a property worth $100,000 it would yield $1,000; $100,000 divided by $1,000 is 100).

That means Australian shares are currently 85% cheaper than Melbourne residential property. How can they be so out of whack? That would make a great dissertation topic for someone far smarter than me, but my hunch is debt has a lot to do with it. In 25 years in financial services I’ve yet to have a client tell me they’d be comfortable gearing a share portfolio to 80%.

Another comparison is M3 Property estimates the current yield on industrial property in Melbourne is 6.25%. Using similar costs as above you’d end up with a net yield almost four times that of residential property, or close to two and a half times the risk-free rate. Again, they seem way out of whack.

A final indicator of how expensive Melbourne’s residential property market is the Annual Demographia International Housing Affordability Survey, which compares how many multiples of median household income it takes to buy the median family home in 293 separate cities across nine different countries (Australia, US, UK, Japan, Hong Kong, Canada, New Zealand, Ireland and Singapore).

Melbourne is ranked as the sixth most unaffordable city (Hong Kong is the worst and Sydney is the second worst). Demographia rates a multiple of more than 5.1 times as ‘severely unaffordable’, and Melbourne’s is 9.9 (Sydney is 12.9).

Australia’s growing pile of household debt

It’s cliched to talk about how much Australians love their property, and it’s reflected not only in how much they’re prepared to pay for it but that they fund those high prices by going into more and more debt.

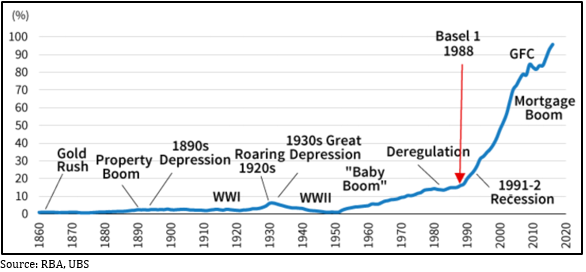

Chart 3 shows the amount of mortgage debt in Australia as a proportion of GDP and clearly shows when housing-related lending activity went parabolic. In 1988 the ‘Basel 1’ banking accord was introduced, which was an international agreement partly designed to make the banking system more stable by prescribing new limits for how much capital banks had to set aside as backing for different types of loans. Australian residential mortgages were considered relatively low risk, which meant the amount of capital required for them was set relatively low, meaning the return on equity for the banks from those loans was relatively high, so not surprisingly our local banks went to town lending to people to buy houses.

Chart 3: Australian mortgage debt as a proportion of GDP

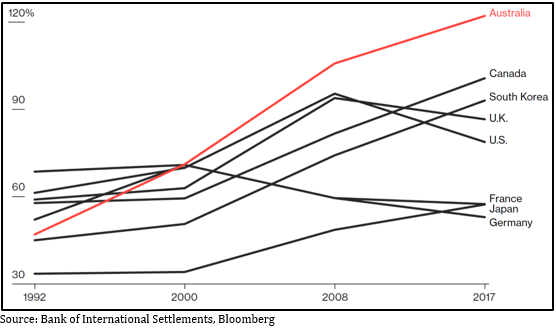

By any measure, Australian households now carry a lot of housing-related debt. The Bank of International Settlements (BIS) ranks Australian households as the second most indebted in the world (behind the Swiss, go figure) and chart 4 compares Australia’s household debt as a proportion of GDP to some other OECD countries and clearly shows the inexorable march upwards.

Chart 4: Household debt as a proportion of GDP

Something that strikes me, US household debt peaked at just below 100% of GDP right before the GFC smashed the property market, now it’s retreated to less than 80%. Ours is currently above 120%.

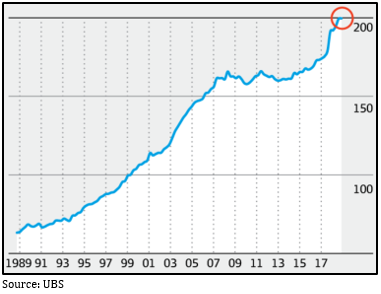

Chart 5 shows another measure: Australia’s household debt to disposable income. The remarkable thing here is it has grown at 10% compoundper annum for the past 30 years. As they say, trees don’t grow to the sky; that is a phenomenal rate of growth in debt and at some point households simply won’t be able to gear up any further – everyone has to spend at least some of their income on living expenses.

Chart 5: Australia’s household debt to disposable income (%)

The interest only problem

When you take out a mortgage to buy a property, there are two components to the loan repayments: the ‘principal’, which is the actual amount you borrowed, and the ‘interest’ you pay on the principal. It’s been popular for property investors to take out ‘interest only’ loans, meaning for (usually) the first five years they only pay the interest costs and none of the principal.

Why would you do that? There are some sound tax reasons around maximising deductible debt, but it also significantly reduces the monthly repayments. For example, if you take out a $500,000 loan at 4.66% it’s the difference between paying $1,942 versus $2,582 per month. Over five years that $640 per month adds up as a lower drain on your cash flow. The problem is of course, after five years you’ve not made any dent in the principal at all.

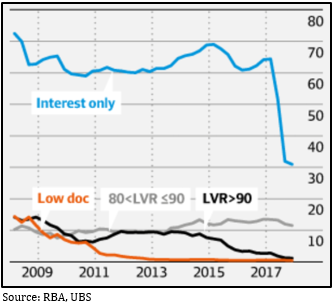

From 2008-2017 interest only loans accounted for about two-thirds of all investment loans and over that time the total amount tripled to peak at about $600 billion. Then in 2017 the Reserve Bank got sufficiently worried about the property market that they instructed the banking regulator, APRA, to cut back the amount of interest only lending. Chart 6 shows the sharp drop off in interest only lending when APRA told the banks to limit it to 30% of all new loans.

Chart 6: the % of interest only investment loans fell away in 2017 after APRA told the banks to cut back

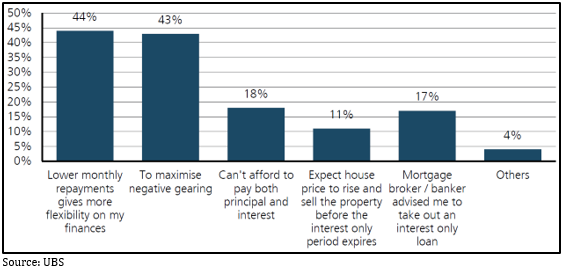

UBS recently did a study on why borrowers took out interest only loans – see chart 7. To begin with, terrifyingly, 5% of respondents didn’t even know whether they had an interest only or P&I loan; but 18% said they opted for interest only because they couldn’t afford P&I and 11% said they intended to sell the property before the loan rolled over to P&I. Also scarily, 17% said they took out an interest only loan because their mortgage broker told them to. All in all, the survey suggests at least half of all interest only borrowers don’t seem to have a solid grasp on what they’re doing.

Chart 7: Reason for taking out an interest only loan

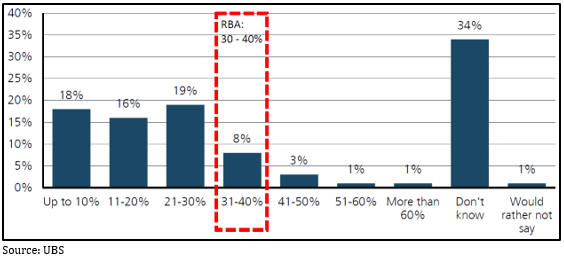

The same UBS survey also asked borrowers how much they thought their loan repayments would increase once it rolled over to P&I – see chart 8. The Reserve Bank reckons the average increase in monthly payments will be 30-40%, but worryingly, more than half under-estimated how much the increase will be, and again concerningly, more than a third had no idea, suggesting they’d not paid anywhere near enough attention.

Chart 8: Borrower’s estimate of the increase in mortgage repayments

The Reserve Bank estimates there’s a total of about $480 billion worth of interest only loans outstanding and $360 billion of those will roll over to principal and interest (‘P&I’) over the next three years. It also estimates that one-third of mortgages have less than a one month payment buffer. If all those numbers line up, that would imply one-third of the $480 billion of interest only loans have less than a one month buffer, so $160 billion worth. Of that, 18% say they won’t be able to afford the 40% jump in loan repayments when the loan rolls over to P&I, which is about $30 billion worth of loans. In a worst case scenario, that could point to a lot of forced property sales.

The banks have tightened credit standards

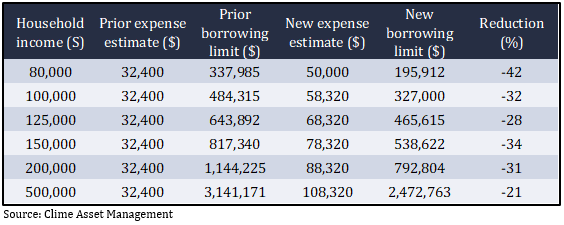

Until recently if you applied for a loan you would have to provide evidence of your income but not your expenditure. If the expenses in your loan application were less than a minimum amount the banks would simply use the so called Household Expense Measurement (HEM), which assumed $32,400 of expenses per year, to work out the amount they’d be prepared to lend to you.

After the recent Royal Commission into the banking and finance industry uncovered dodgy lending practices, the banks have been moving to tighten things up. Now they’re starting to require verification of both income and expenses, insisting on seeing things like bank and credit card statements. The upshot is the amount the banks are prepared to lend is estimated to drop by between 20-40% from previous levels – see chart 9.

Chart 9: New estimated borrowing limits based on revised expense estimates

Obviously, that simply translates into less money people can spend on buying a property, which you can only presume will feed straight into lower prices.

The washup

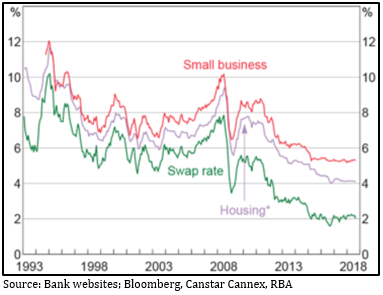

I know there have been calls for years that Australian housing is overvalued and dire predictions that our banking system is overexposed to it. I’m not making any such forecasts, I’m simply pointing out that there’s a limit to how much debt Australian households can take on to buy a house. Chart 10 shows the general trend of Australian mortgage rates has been downward for the last 25 years, which has underwritten a steady increase in borrowing capacity. If interest rates have indeed bottomed, will that cycle reverse?

Chart 10: Australian fixed interest rates have been on a downward trend for 25 years

The Reserve Bank has kept cash rates at a record low of 1.5% for more than two years and there’s no sign they’ll be raising them any time soon. However, Australian banks source a lot of their funding from offshore and rates there have already started to move upwards. We’ve already seen three of the big four banks raise mortgage rates a couple of months ago and there’s every chance they will do the same again. When borrowers are so stretched any tweak to rates has a very real effect.

I should emphasise, I’m not forecasting a crash in housing prices, there are a lot of arguments that the majority of Australian borrowers are well positioned to weather a downturn (though sometimes it’s hard to unravel where those arguments might be pushing someone’s barrow). Also, the Reserve Bank is acutely aware of how important the housing sector is to the overall Australian economy and will almost undoubtedly move to support it if necessary, and as the market adage goes, it’s unwise to argue against a central bank. What I am wondering is how sustainable the increase in household debt is, and if the answer is it has to slow, stop or even reduce, then what happens to house prices?

There has been a lot of media around the findings of the recent royal commission and how the banks have now made it significantly harder to apply for a loan. Another change, that was mandated prior to the royal commission, is set to place a much greater importance on keeping your credit file squeaky clean.

Most people who apply for a loan, from a mortgage to a credit card, accept that the lender will perform a credit check on them. Whilst these credit checks have always played a significant role in whether the application was accepted or declined the data that was historically available was limited to three items:

The date of the last credit enquiry for the applicant.

The name of the credit provider that made the inquiry, e.g. ANZ bank

If there were any credit defaults or bankruptcy registered against the applicant. A credit default includes a repayment in arrears for a period of 60 days or more.

The lender would then rely on the applicant to include the balances and structure of any outstanding loans in their application and back them up with the relevant statements.

On 2 November 2017 the government announced it would legislate for a mandatory Comprehensive Credit Reporting (CCR) regime to come into effect by 1 July 2018. So by 1 October 2018 the four major banks were required to report that 50% of their credit data, including home loans, credit cards, car leases, etc. are shared with a credit bureau and made available to other industry participants. By 1 October 2019 this figure will grow to include 100% of all credit data.

Whilst the government’s mandate only applies to the four major banks, to gain access to the data a lender must also be a participant so it’s expected the smaller lenders will follow.

What does this mean?

Under the new reporting regime, the number of data points contained in a credit file would be significantly increased. In addition to the three listed above, the information available to lenders would include far more detail around the balance and limit of any loans you have outstanding or closed, the type and structure of those loans and their month by month payment history for the previous two years.

All these factors will then be considered to produce a credit score for the applicant of between 0 and 1000. Clearly this will provide lenders access to a lot more data, enabling them to better assess a borrower’s true credit position and hence their ability to repay a loan.

How will this affect me when applying for a loan?

As more Comprehensive Credit Reporting (CCR) information becomes available, it should drive competition and result in lenders offering a better deal based on your unique credit circumstances. In short you could be rewarded for a good credit score with a lower interest rate or punished for a bad one. The race will be on to best utilize this level of data and introduces the possibility of nimble fintech start-ups to enter the marketplace.

It may also result in a reduction in the documents you need to provide the lender with your application. If a lender can view your current balances and repayment history, then there may not be a need to provide this information in the form of paper statements.

Whichever way you look at it, the change will place far more importance on maintaining a clean credit file and will ultimately result in a more competitive risk adjusted lending market.

Most people don’t apply for a home loan many times in their life. Even if you’re just renovating or refinancing, it may have been 3–10 years since you last applied for a home loan and there have been a lot of changes in the lending market over that period so that what used to be a relatively straight forward application process can now be a frustrating, and potentially costly, experience.

What has caused the changes in the market?

In 2014 the Reserve Bank got concerned about the sharp rise in house prices and requested APRA, the government watchdog for the banks, to tighten the ‘prudential’ lending regulations and hopefully slow the market, so APRA limited the banks to a maximum of 10% growth in investor lending over a 12-month period.

To meet these new requirements the banks raised interest rates on investment loans in some cases by as much as 1% almost overnight, as well as significantly tightening their loan application assessment policies. Chart one shows the impact that this has had on the growth rate of investor lending.

Chart1: Investor lending slowed sharply after APRA tightened regulations

Source: JP Morgan

Then in April 2017 APRA introduced additional macro-prudential measures which capped interest-only lending at 30% of all new loans issued. Around six months after that was introduced, home prices in Australia’s major east-coast housing markets began to decline. Chart two shows the significant fall in year on year house prices in Sydney and Melbourne particularly.

Chart 2: Melbourne and Sydney home prices started to decline after APRA restricted interest-only loans

Source: JP Morgan

Throughout this period APRA has also been working closely with banks to develop stricter underwriting standards for both investor and owner-occupied loans. This tightening, combined with the public shaming at the Royal Commission into Financial Misconduct, has forced banks to take note.

How has this affected the lending process?

There is no doubt the regulatory changes have been introduced to make sure our financial system remains unquestionably strong, however, for anyone intending to apply for a home loan there are consequences you should be aware of.

1. More paperwork – In the past lenders have been able to accept that what you entered on your application was correct, but today they will require you to verify much more of your financial situation with documentary evidence in the form of bank statements. Often the submission of one statement leads to further requests which can be frustrating for all involved.

2. More questions – Banks are required by their regulators to keep evidence explaining why they assessed your application in a certain way. While something may seem obvious to you as the borrower, the banks may request an explanation in writing to ensure they have documentary evidence.

3. Living expenses – Currently banks ask that you estimate your living expenses and then take the higher of your estimate or the Household Expenditure Method (HEM). HEM is a national standard based on a few things, including where the borrower lives and the number of dependent children, and then assumes a basic standard of living. History has shown borrowers generally have a surprisingly vague understanding of their monthly living expenses and tend to underestimate this figure, and banks are now starting to require more evidence in the form of transaction or credit card statements to prove actual expenditure, rather than simply taking an estimate. A review of the HEM model is also underway.

4. Inflexible – Each bank has a list of criteria that need to be met to gain loan approval and these are documented in the bank’s lending policy. Banks have been instructed by APRA to strictly adhere to these policies and make very few exceptions. As a result we have seen an increasing number of declined applications for circumstances that may seem like common sense to the borrower, but unfortunately do not meet the specific requirements of the lender’s policy guide. Each bank’s policy guide is different, and it pays to speak to someone who has knowledge of these subtleties.

5. Principal and Interest (P&I) repayment – with such a regulatory emphasis on investment and interest only loans, it doesn’t take much to realise that much of the recent lending growth has come in the form of P&I repayment. Depending on your personal circumstances and lending objectives, you may consider paying principle and interest (P&I) instead of choosing an interest only loan.

These are just a few examples in which applying for a home loan has become significantly more difficult in recent times, but they highlight the importance of speaking to a professional to ensure you have the right structure and preapproval before you make an offer on a property. Where appropriate, we can also help you to apply with a non-bank lender that is not affected by APRA’s restrictions.